Note: The math and taxes underlying this have a ton of different knobs and nuance, so I’ve made some simplifications1. The examples are meant to get the point across and be illustrative of potential outcomes. Nevertheless, you shouldn’t take this as advice, crunch your own numbers to see what makes sense for you

Let’s take two people, Kevin the Keeper and Gordon the Giver. They have an adjusted gross income (AGI) of $100k/yr and are single. Gordon took the 10% Giving What We Can pledge in 2013, and uses his AGI as the basis, targeting donations of $10k per year which he will make in cash.

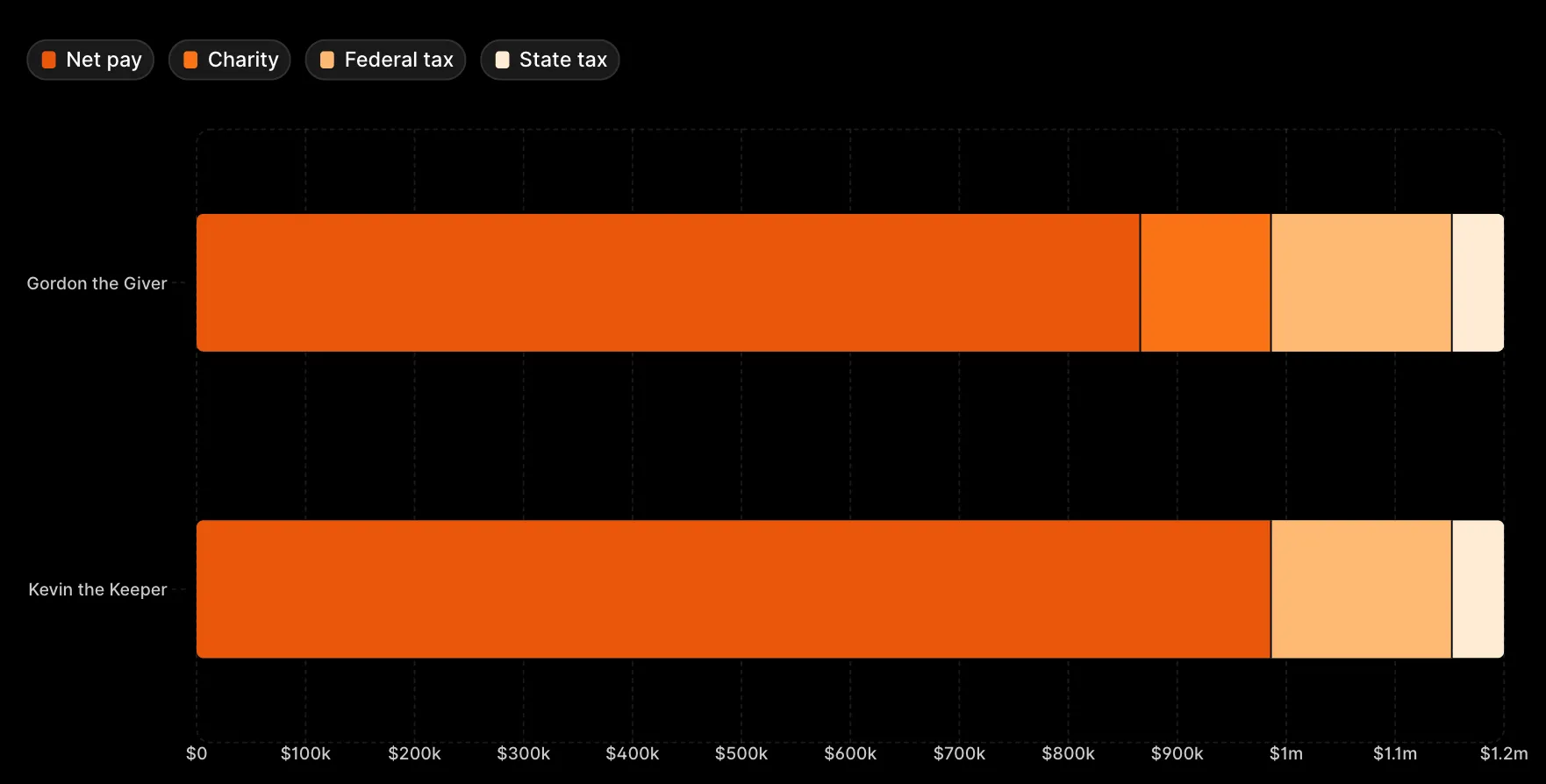

Let’s assume their state and local taxes are $4k. They both take the standard deduction and wind up paying about $13.9k in taxes. Kevin kept all his money, but paid the same2 in tax!

Here’s how it looks after 12 years:

Raw data

| Net Pay | Charity | Federal Tax | State Tax | |

|---|---|---|---|---|

| Gordon the Giver | $866k | $120k | $166k | $48k |

| Kevin the Keeper | $986k | $0 | $166k | $48k |

The tax code incentivizes charitable giving, but it can require some maneuvering. Here I’ll outline one approach, starting with the tools/concepts, then show how they come together like a financial Megazord.

But first we’ll add in Dave the Deductor. Dave takes the GWWC pledge with Gordon, except he wants to minimize his taxes3.

Donation Bunching

As seen earlier, donations that occur below the standard deduction ($14.6k for singles) are “wasted” since it doesn’t directly reduce tax burden. Because of this, Dave needs to bunch together donations within a single year. This will allow him to itemize his deductions and get the bulk of the donation written off.

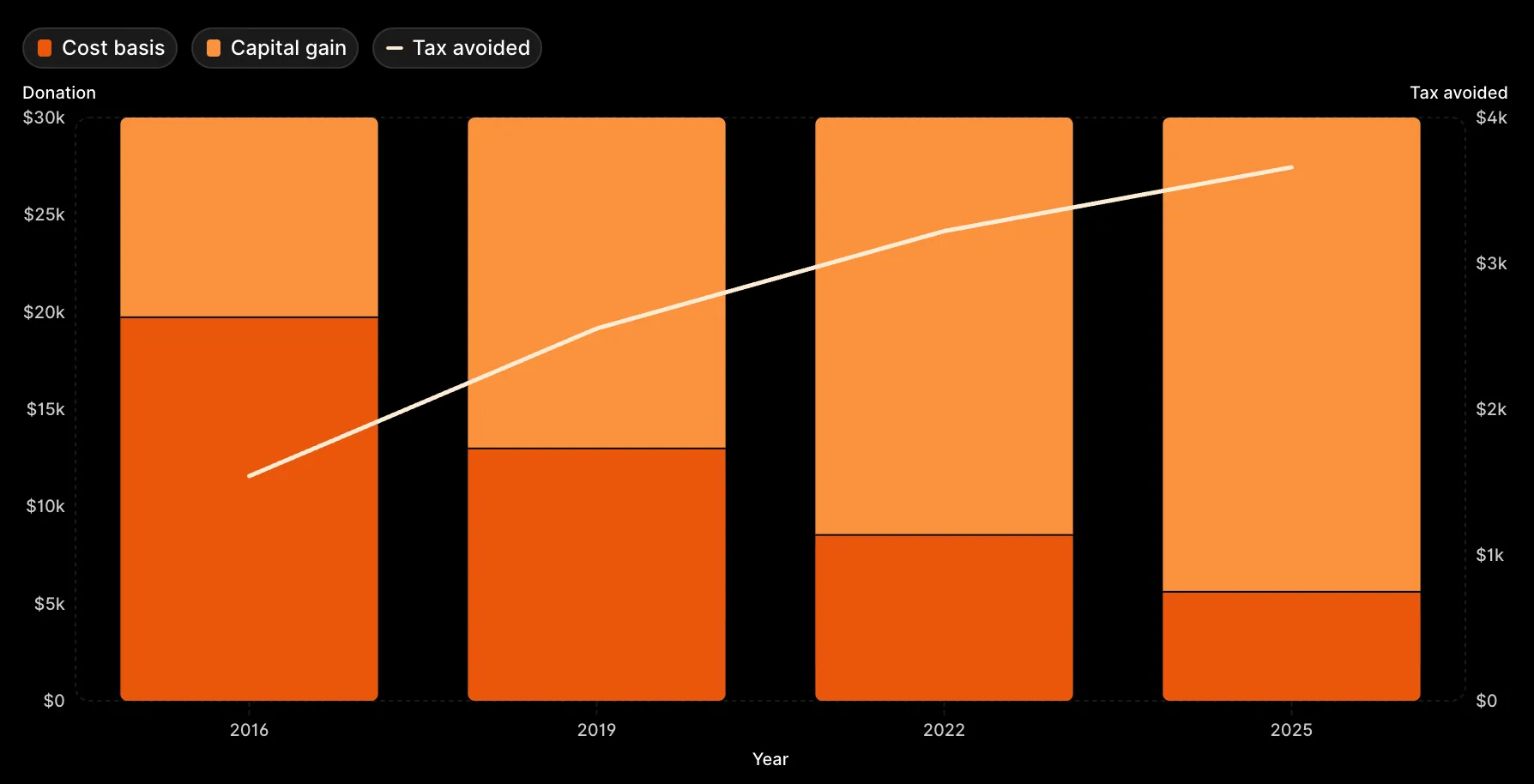

Dave decides that rather than giving $10k/year, he will give $30k every 3 years4. During those years, he’ll be able to itemize his deductions and wind up owing about $10.5k in federal tax. His four giving tranches in our 12 year timeframe (2016, 2019, 2022 and 2025) each alleviate ~$3.4k in tax, yielding ~$13.6k total.

Itemization also unlocks the state and local tax (SALT) deduction. Using the assumed $4k SALT from earlier at the 22% marginal rate, this avoids another ~3.5k across the four tranches ($880 per year).

The Donor Advised Fund (DAF)

A Donor Advised Fund sounds all high-falutin’ but it’s basically just a financial instrument that decouples the timing of a donation’s tax event (when money leaves your account) from the actual granting (when money goes to the charity). This is useful if your employer has an annual giving match, since it lets you reap the benefits of bunching (through lump contributions) while keeping the matches (through annual grants)5.

Another important feature of DAFs is that you can directly transfer assets to them, e.g. stocks, without triggering a sale (known as an in-kind contribution).

Most major brokerages make it easy to set up a DAF, like Fidelity and Vanguard. They all come with management fees, which are typically low.

Donating Appreciated Assets

When contributing assets in-kind to a DAF, the entire value of the asset is tax deductible. That is, if you bought a stock for $1 and it grows to $100, you can write off that entire $100.

Let’s say that all three of our characters had $100k in an S&P 500 fund ($SPY) at the start of 2013 (for now we’ll ignore any subsequent contributions). From 2013 to 2025 the market has done insanely well, with $SPY averaging over 18% in gains per year. We’ll use 15%, still high but less insane. Let’s also assume a 15% long term capital gains (LTCG) tax rate which we’ll use to calculate how much future taxation Dave may avoid over Gordon by donating now rather than selling later.

Here’s what Dave’s bunched donations look like under those assumptions:

Raw data

| Donation Year | Cost Basis | Capital Gain | Tax Avoided |

|---|---|---|---|

| 2016 | $19,727 | $10,273 | $1,541 |

| 2019 | $12,979 | $17,021 | $2,553 |

| 2022 | $8,528 | $21,472 | $3,221 |

| 2025 | $5,607 | $24,393 | $3,659 |

| Total | ~$47,000 | ~$73,000 | ~$11,000 |

As the investment compounds, the donation shifts increasingly to capital gains, strengthening the financial benefit. The charity, as a nonprofit, doesn’t pay tax on the gains either.

Tax-loss harvesting (TLH)

But wait, there’s more! When stock is sold for less than the cost basis, it results in a capital loss. That loss can be used to offset capital gains, or $3k per year of ordinary income. Income is a better target to reduce since it’s generally taxed at a higher rate than capital gains.

Dave can’t just sell $SPY when it goes down then turn around and buy it back (that’s called a wash sale). Instead he has to buy something that’s not “substantially identical”, such as $VTI. But what does this have to do with charity? Well TLH lowers the cost basis of holdings, so if you were to take $20k in losses and buy back in, you’ll have $20k in unrealized gains that will be subject to tax when you sell, limiting the benefit. But Dave can donate those appreciated shares in-kind through his DAF, so the lower cost basis doesn’t matter!

Determining the effects of all this is a bit complicated, so let’s just assume that Dave is making periodic investments in $SPY, and during the dips in the market he was able to realize $12k in losses. He uses this to write off $3k/year against his ordinary income for four years. At his marginal rate of 22%, this avoids another $2.6k in tax.

Putting it all together

Here’s the final game plan:

- During market downturns, Dave sells any $SPY holdings that have fallen in value and buys back in via $VTI (or vice versa), realizing the losses.

- Every 3 years, he contributes $30k of his most highly appreciated assets to his DAF, benefiting from (but not realizing) the gains.

- He periodically repurchases $SPY, locking in a higher basis and increasing the likelihood of future tax-loss harvesting opportunities.

- He grants funds annually from his DAF to get matching funds from his employer.

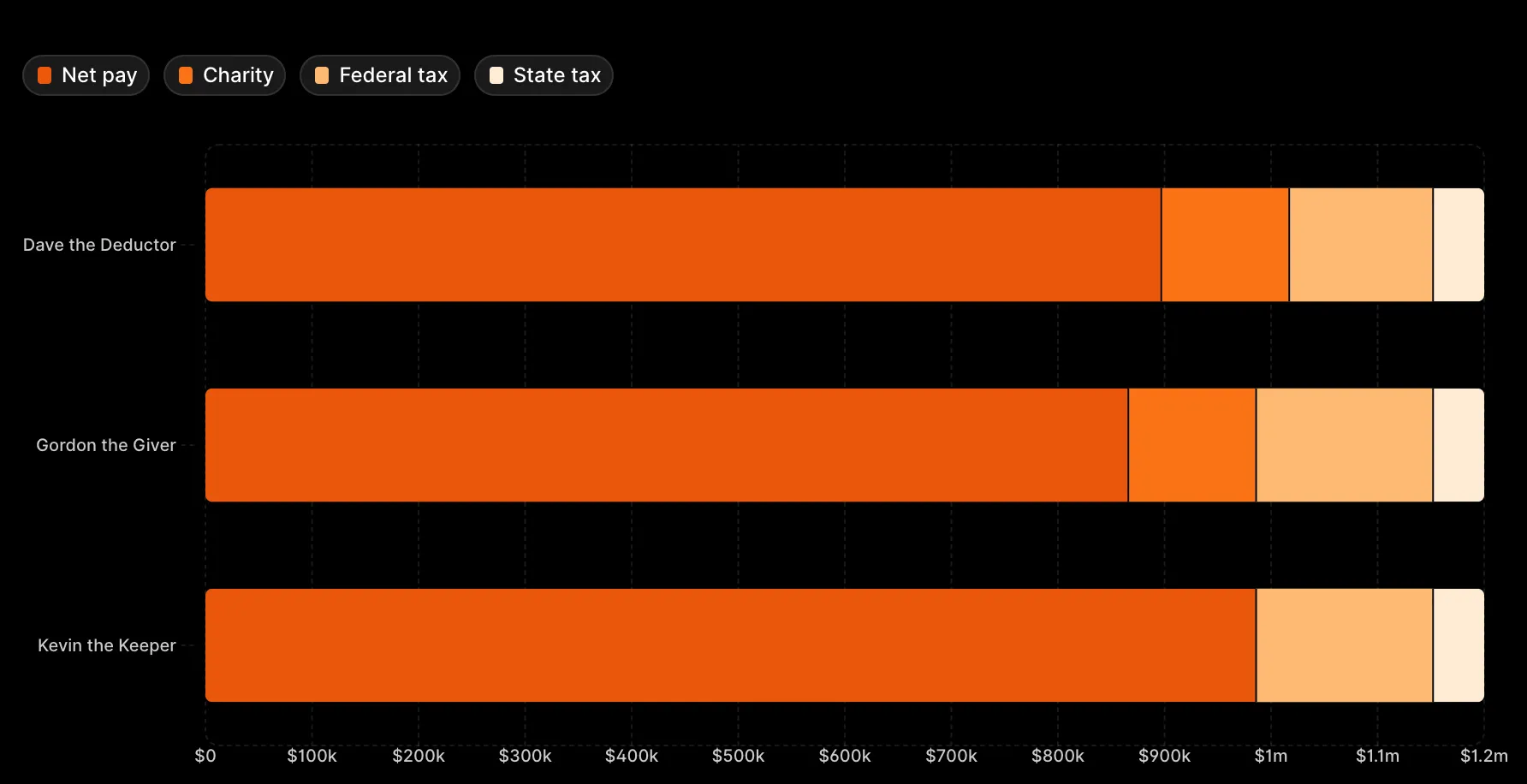

All told, he avoids $13.6k (bunching) + $3.5k (SALT) + $11k (avoiding LTCG) + $2.6k (TLH) = $30.7k. That’s pretty efficient, representing an ~25% “rebate” on the $120k of total giving, and the strategy will grow in effectiveness over time as the leftover assets appreciate.

Bearing the aforementioned nuances in mind, here’s the final tally:

Raw data

| Net pay | Charitable donations | Federal Tax | State tax | |

|---|---|---|---|---|

| Dave the Deductor | $897k | $120k | $135k | $48k |

| Gordon the Giver | $866k | $120k | $166k | $48k |

| Kevin the Keeper | $986k | $0 | $166k | $48k |

If you’d like to play around with your own numbers, here is a vibe-coded calculator. Unlike the numbers in this post, I didn’t rigorously verify the math within the tool so take them with a grain of salt.

Footnotes

-

Rounding, ignoring historical/future changes to the tax code (basically just treating every year using the 2024 tax code), ignoring inflation and raises, and ignoring interest and the time value of money ↩︎

-

Starting in the 2026 tax year the OBBA would allow Gordon to deduct $1,000 per year without itemizing ↩︎

-

To be clear I don’t intend this post as a normative (much less moral) statement, but as an explainer for a set of optional tax maneuvers ↩︎

-

Why three years? You’re limited to deducting 30% of AGI per year through in-kind donations like those mentioned later, and doing 3x10% is an easy way to stay within that limit. For cash the limit is 60% of AGI, so if you plan to remain in the 0% capital gains bracket (e.g. if you will have a relatively frugal retirement), and want to purely focus on minimizing income tax, then in this specific case a 5 year cycle of $30k in assets and $20k in cash wins out ↩︎

-

Not all employers accept DAF grants for matching, so check first. If your employer doesn’t do matching then this decoupling may not be necessary, since it’s possible to donate assets directly. However, that depends heavily on the combination of brokerage, assets, and charity, making a DAF the more general-purpose option. Additionally, DAFs allow for periodic small donations instead of infrequent lump sums, which some charities prefer. ↩︎